I frequently hear advisors who are proponents of long-term

care planning say:

•

“I would be remiss if I didn’t bring it up with

every client.”

•

“Not bringing it up is negligent and setting clients

up for financial catastrophe.”

•

“It’s too big of a risk to ignore in the planning process.”

•

“It could blow up their entire retirement plan.”

•

“It is my fiduciary responsibility to have every client

prepare for this possibility.”

On the other hand, advisors who aren’t yet on board with

the idea often say:

•

“My clients don’t need it.”

•

“It’s too hard to sell.”

•

“I’m uncomfortable engaging in the long-term

care conversation.”

•

“It’s too expensive.”

•

“It’s not worth my time.”

I can certainly understand the arguments on both sides,

but I would argue (how could I not, as a long-term care

product manager?) that long-term care planning is vital

to clients’ financial health. Of course, having the discussion

with clients is often easier said than done. If you’re not

sure where to begin, this four-step approach can help you

incorporate long-term care planning into your practice:

1.

Believe

2.

Commit to action

3.

Master the conversation

4.

Tap into the Insurance department’s resources

Believe

In order to talk convincingly with your clients about

long-term care planning, you first need to believe that

it’s a critical component of their financial plans. Most

advisors plan well for the inevitable death of a client,

but it’s just as important to plan for old age. Without

a long-term care plan, a client risks significant financial

loss due to health care costs.

Keep in mind that all of your clients already have a

long-term care plan in place. How is that? Well, in the

absence of a long-term care insurance (LTCI) policy,

their plan is to spend their own income on long-term

care expenses. Your plan, in the absence of an insurance

policy, is to counsel them at the time of a long-term care

event on the least damaging way to reallocate their

income to cover those expenses.

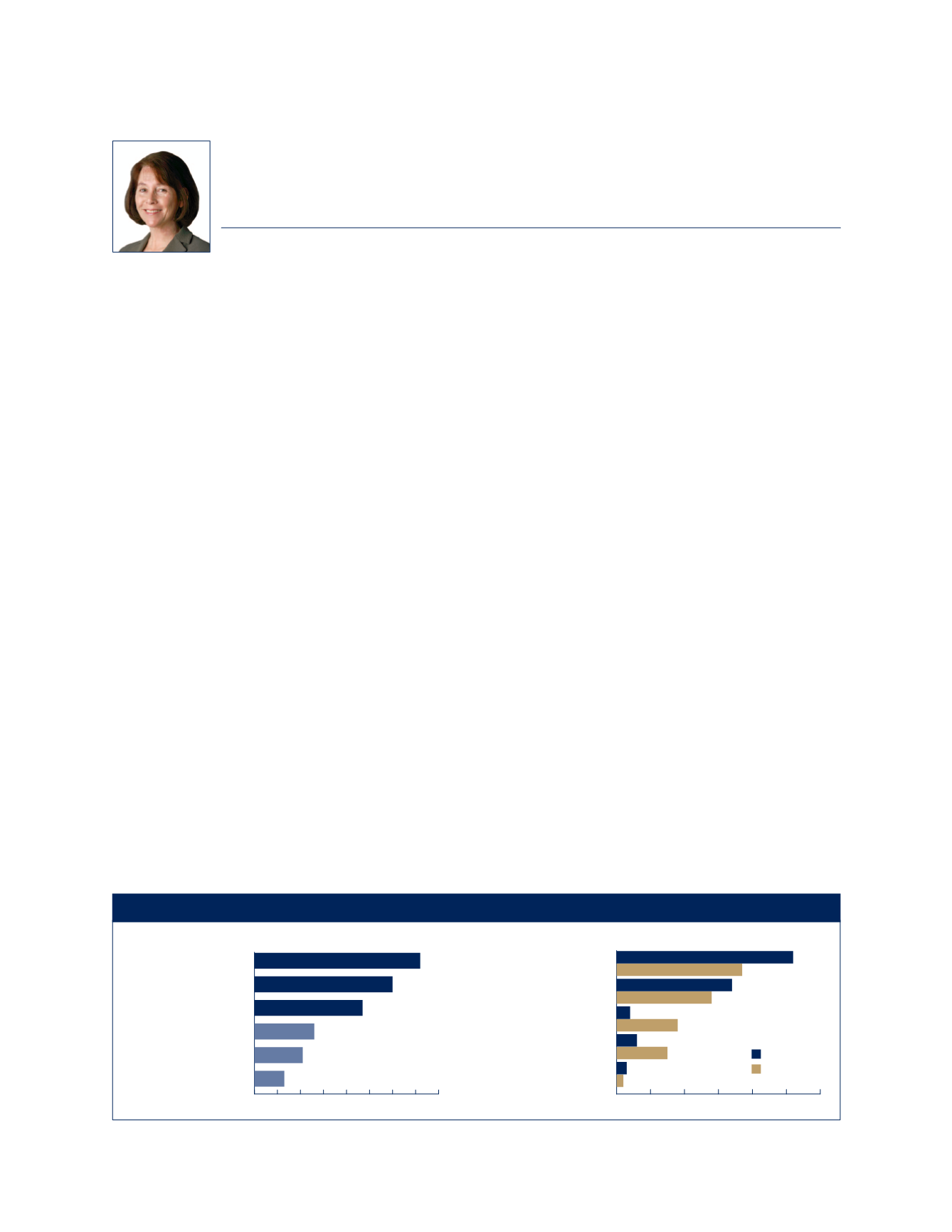

It is generally assumed that clients’ biggest worry is

running out of money. A 2013 Merrill Lynch retirement

study, however, revealed some surprising responses to the

questions “What is your number-one retirement worry?”

and “What are your top financial worries for retirement?”

(see Figure 1).

commonwealth.com

For Advisor Use Only

7

Wealth Management

/ Insurance

Overcoming Commitment Issues: A Four-Step Process for

Eliminating the LTC Wild Card in Clients’ Retirement Plans

SUSAN KOBARA, CLTC

Long-term care planning can be a

controversial topic, generating enthusiastic

discussion and debate among advisors.

0% 10% 20% 30% 40% 50% 60% 70% 80%

0% 10% 20% 30% 40% 50% 60%

52%

72%

60%

47%

26%

21%

13%

37%

34%

28%

4%

18%

6%

15%

3%

2%

Serious health problems

Biggest worries about living a long life

Top nancial worries about retirement

Being lonely

Not having a purpose

Health care expenses

Outliving my money

Lack of personal savings

Lack of social security

Lack of company pension

Not being a burden

on my family

Running out of money

to live comfortably

Having nothing left to leave

my children/grandchildren

Above $250K

Below $250K

Population by

Investable Assets:

Source: Merrill Lynch, “Americans’ Perspectives on New Retirement Realities and the Longevity Bonus”

Figure 1. Health Problems: The #1 Retirement Worry