The Municipal Fund Trade

In addition to spending time on allocation decisions, the

PPS Select team devotes significant effort to making what

we believe are the right fund selections. An example of

how we do this took place in October 2012, when we

replaced a long-standing municipal bond fund.

This was a fairly contentious decision for us because the

original fund had delivered excellent performance over

the previous few years. Because of its longer-than-average

duration and higher portfolio concentration, the fund’s

management team had been successful in riding both the

decline in rates and the tightening of spreads between high

and medium credit-quality issuers.

Despite the fund’s successes, however, one team member

pointed out the risks associated with a long-duration,

lower-quality-oriented portfolio. From a contrarian

perspective, a recent decline in rates and tightening of

spreads had made these areas less attractive. The fund

also had a history of either performing in the very top

few percentiles of its peer group or in the very bottom.

For these reasons, he argued that it made sense to sell

the fund at the top. Other members of the team were

skeptical at first, but the evidence suggested that a change

did indeed make sense.

After culling the universe of municipal bond funds and

organizing meetings with a variety of portfolio managers,

the team settled on the

Franklin Federal Tax-Free Income

Fund (FAFTX)

as a replacement. We liked that the fund

had a history of conservative, consistent management under

the watch of a tenured and stable team. Its duration was

more than a year shorter than our original manager, the

credit quality tended to be a bit higher, and the portfolio

was more diversified.

Over the next couple of months, interest rates moved

lower, helping the relative performance of our original

fund and hurting the performance of our replacement.

Had we erred in making the switch? Because we had

thoroughly vetted the decision and agreed as a group to

make the trade, we avoided the temptation to admit

defeat and alter the portfolios again.

And the team’s solidarity ultimately paid off. As the interest

rate environment changed during 2013, the new fund

held up better in the face of asset class-level headwinds.

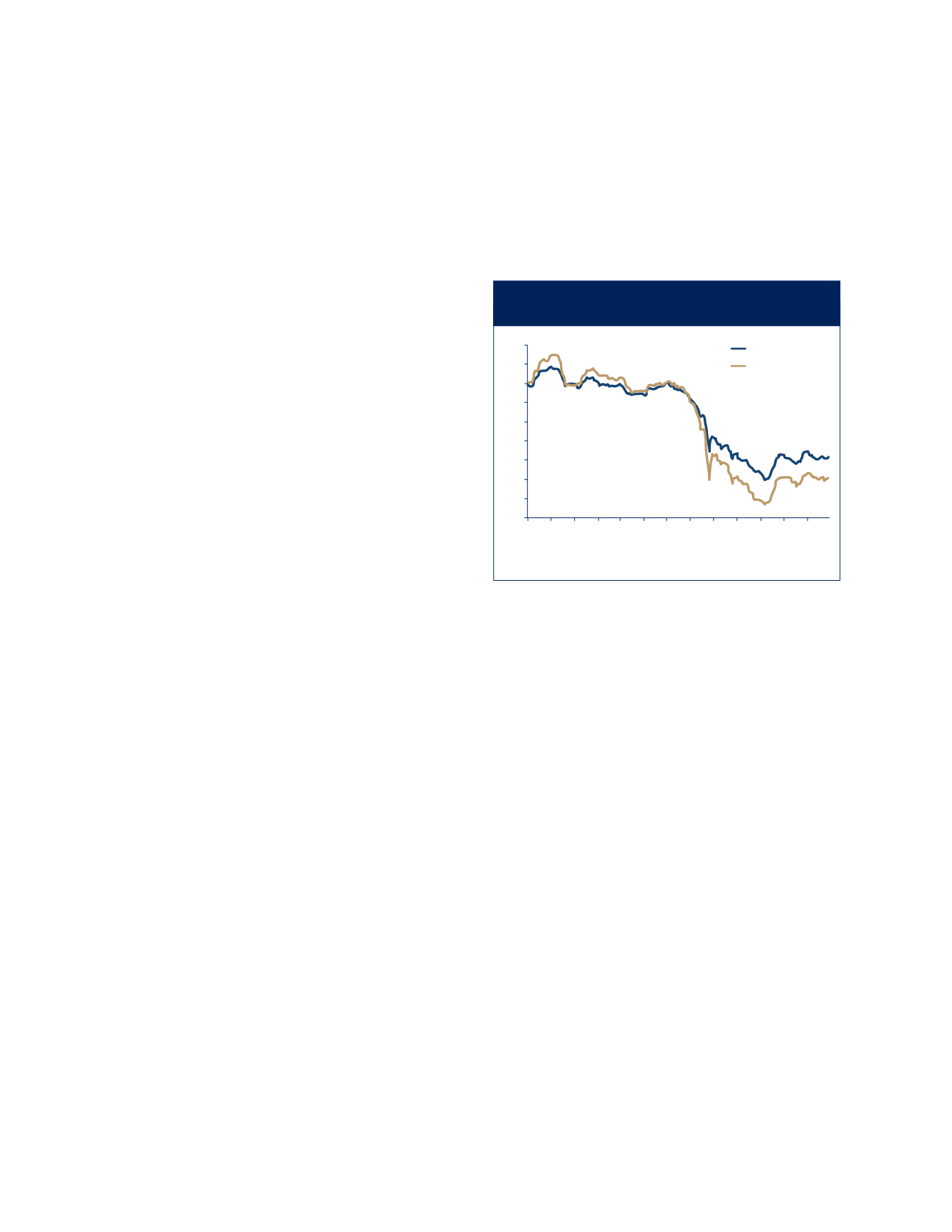

One more note . . . looking at Figure 2, some might ask

why we maintained exposure to the asset class at all. We

accept and understand that, in most market environments,

some portion of our portfolios will have a tendency to

underperform. We see this as a positive. It means that the

portfolios are diversified with assets that have low correlations

to one another. Although the municipal bond portion of

the portfolios struggled in 2013, strong equity market

performance helped the portfolios gain ground overall.

The International Trade

Since before the financial crisis, the PPS Select team had

maintained an underweight to developed international

equities. This was primarily due to our concerns about the

economic and political situation in Europe, as well as our

relatively more optimistic view on prospects here in the U.S.

But our calculus began to change in mid-2012, when

European Central Bank President Mario Draghi pledged

to support the euro at any cost. Another major factor was

commonwealth.com

For Advisor Use Only

21

FAFTX

Previous Fund

104

102

100

98

96

94

92

90

88

86

10/31/12

11/30/12

12/31/12

1/31/13

2/28/13

3/31/13

4/30/13

5/31/13

6/30/13

7/31/13

8/31/13

9/30/13

10/31/13

Source: Bloomberg

Figure 2. Franklin Federal Tax-Free Income Fund Vs.

Previous Holding, October 2012–November 2013

Wealth Management

/ Investments & Research