24

For Advisor Use Only

January/February

2014

The Impact of Underpricing

After this brief review of industry data, maybe you are

ready to reassess your fee schedule. But how do you begin?

Let’s start by looking back at Figure 1 and considering

the tiers with the higher dollar amounts—$2 million and

up. If you underprice in these areas, it doesn’t really hurt

your business because managing these accounts at almost

any price is likely to be fairly profitable. A $4 million

account for which you charge 72 basis points, for example,

earns you $28,800 a year. For $28,800 annually, you

could spend a significant amount of time on the account

and provide your client with a lot of service while still

remaining profitable.

But if you focus on the lower-tier amounts—specifically

on the accounts valued at under $1 million—you can see

where underpricing could have a real impact on your

business. And these are the tiers in which the majority of

Commonwealth advisors’ accounts fit. You need to get

the pricing right here, as these accounts are drastically less

profitable, though probably just as much work to service,

compared with the larger accounts.

Take an account worth $200,000 for which you charge

a 1-percent fee to manage. This means that your annual

fee is $2,000. If you are worth $250/hour—and I would

contend that Commonwealth advisors are worth more,

based on their credentials and experience—that is eight

hours a year of work to remain profitable. If you add up

the number of hours you spend in meetings, prepping,

researching, and talking with clients annually, on average,

do you come up with more than eight hours? I bet that

most of you do.

So if you would like to make a pricing change, this is the

client tier you should target.

The Blended Approach

One way to increase the profitability on smaller accounts

is to switch to a blended fee schedule. Most advisors at

Commonwealth use a breakpoint schedule. In my opinion,

breakpoint

is a commission term—like the breakpoints

associated with A-share mutual funds.

A

blended schedule

is more of the industry standard. It’s

what institutional money managers and separate account

managers use. Let’s compare two almost identical

schedules—one a breakpoint and one a blended

option—as illustrated in Figure 2.

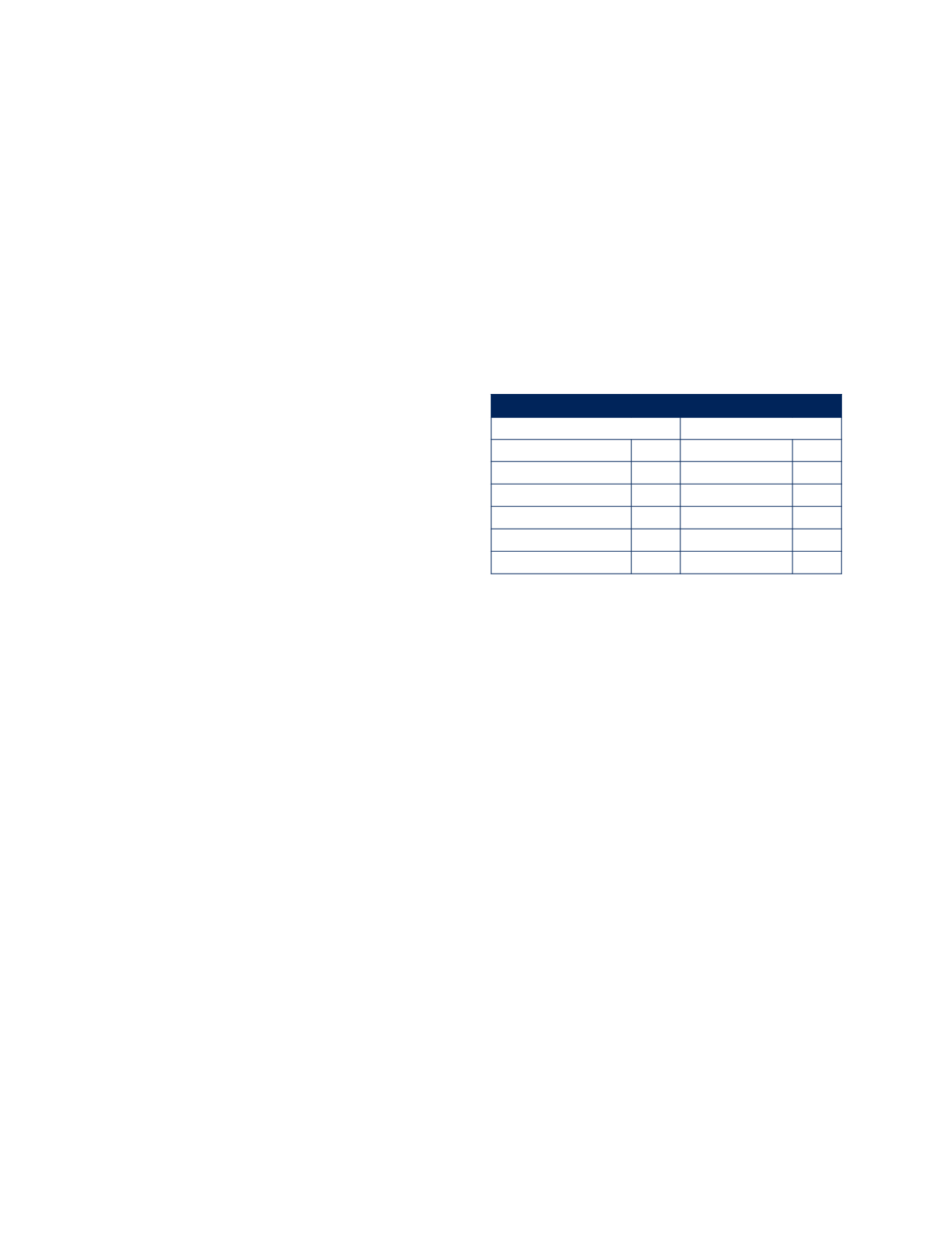

Figure 2. Breakpoint Vs. Blended Fee Schedules

Breakpoint

Blended

AUM

Fee AUM

Fee

Less than $500,000

1.15% First $500,000

1.15%

$500,000–$1,000,000 1.00% Next $500,000

1.00%

$1,000,000–$2,000,000 0.90% Next $1,000,000 0.90%

$2,000,000–$5,000,000 0.80% Next $3,000,000 0.80%

$5,000,000+

0.55% $5,000,000+

0.55%

Source: Commonwealth

At an initial glance, could a client even tell the difference

between the two schedules? They look pretty much the

same; however, with the breakpoint schedule, if you do

some simple calculations, you’ll find that your revenue

could drop even as the value of the account increases.

Suppose you handle a $995,000 account and use the

breakpoint schedule in Figure 2 to charge for your services.

Your fee will be 1 percent or $9,950 annually. If, over the

course of one year, the account value were to increase by

$5,000 (or slightly more than 5 percent) to $1 million,

your fee would actually drop, to $9,000 (0.90 percent

x

$1 million). So, even though you would have done a good

job and helped the client’s assets grow, your revenue would

drop more than 9.5 percent because of your fee schedule. It

is a flawed way to price the value of your expertise and labor.

If you were to use a blended schedule, however, your fee

for managing the $995,000 account would be $5,750 on

the first $500,000 and $4,950 on the next $495,000, for

a total of $10,700. If the account value were to rise to

$1 million, your fee would be $5,750 on the first

$500,000 and $5,000 on the next $500,000, for a total

of $10,750. So you would do better in both cases.

Wealth Management

/ Investments & Research