commonwealth.com

For Advisor Use Only

17

Wealth Management

/ Insurance

At this stage of life, debt combined with dependents creates

a significant and often unmet need for life insurance. The

32-year-old with two kids, a mortgage, student loans, and

529 and 401(k) plans to fund faces a host of obligations

contingent on his or her ability to earn an income. From

an insurance standpoint, the value of the client’s life is at

its peak, yet he or she may have little to no coverage. These

clients need more life insurance, and you could be their

only hope of getting it.

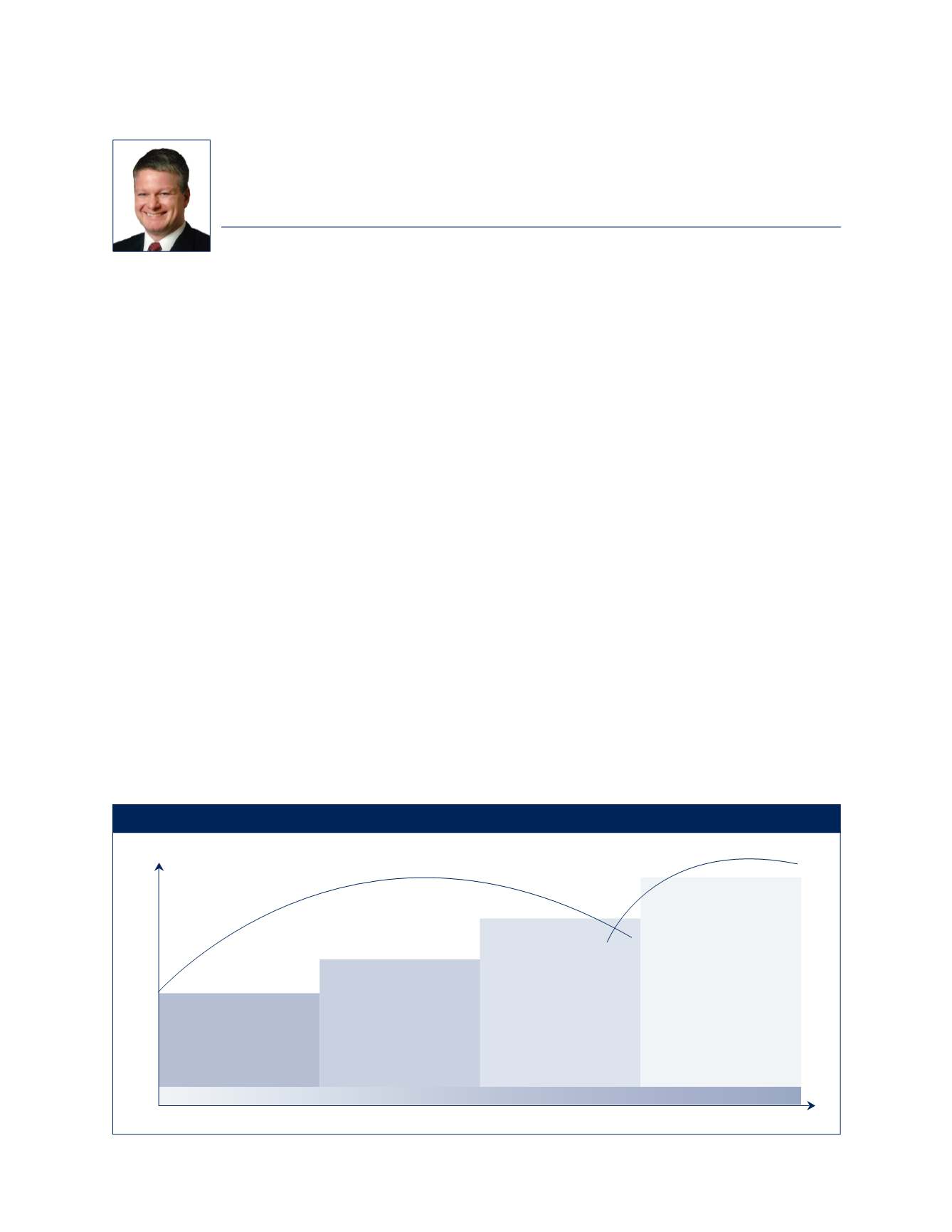

Are Your Clients at Risk?

Clients’ evolving coverage needs can be illustrated with two

arcs, as shown in our Who Depends on You? client-approved

marketing piece (see Figure 1). The larger arc rises with

increasing responsibilities to home, family, and business

as the client proceeds through life. As the client nears

retirement, a second, smaller arc rises, representing the

potential desire to leave a legacy through wealth transfer.

At the peak of the first arc, recent studies have shown, clients

are woefully underinsured and realize they need coverage;

they just need someone to help or ask for the business.

Consider these startling facts from Genworth’s

2012 LifeJacket Study

:

•

Of Americans with household incomes between

$50,000 and $250,000, 44 percent do not have

life insurance. (That’s 53 million people without

life insurance.)

•

Even for those who do own life insurance, the average

amount of coverage is only $152,000, offering just

a few years of income replacement at most.

•

43 percent of married mothers lack life insurance,

compared with 34 percent of married fathers.

Combine these statistics with the fact that 50 percent

of U.S. households say they need more life insurance

(according to LIMRA’s

Facts About Life 2013

), and

you have a population with substantial and potentially

disastrous risk.

Why It Matters for You

If you work primarily with pre-retirees and retirees on the

other side of the arc, it’s easy to dismiss this risk as not

Meeting Clients’ Life Insurance Needs at the Top of the Arc

BRIAN HARRISON, CFP®, CLU®, CHFC®, CLTC

When it comes to planning for retirement and other goals, advisors often hear

about taking advantage of a client’s “peak earning years.” Rarely, however, do

you hear about the “peak debt years,” which typically arrive in a client’s 30s.

RESPONSIBILITY

TIME

Self

Term Insurance

Disability Insurance

Liability Insurance

(Auto, Home/Renters Insurance)

Spouse/Family

Life Insurance

(Term or Permanent)

Disability Insurance

Liability Insurance

(Auto, Home/Renters Insurance)

Home/Family/Business

Disability Insurance

Life Insurance

(Term or Permanent)

Long-Term Care Insurance

Liability Insurance

Property and Casualty Insurance

Umbrella Insurance

Building a Legacy

Survivorship Life Insurance

Long-Term Care Insurance

Getting Started

Retirement

Figure 1. Who Depends on You?