Wealth Management

/ Insurance

18

For Advisor Use Only

March/April

2014

your problem. But think about it: who will these exposed

millennials and Gen Xers depend on if they lose an income?

Likely, just as it was when they moved home post-college,

it’s your clients.

Fortunately, covering clients in this demographic with term

life insurance can be easier—and more profitable—than

you might think. Consider the average term premium of

$1,200 per client. With payouts up to 100 percent, a married

couple with equal coverage could generate a $2,400

commission. And with Commonwealth’s Insurance team

here to quote, prequalify, fill out paperwork, and usher a

case through to delivery, you stand to earn more than your

hourly rate to write that “unprofitable” term insurance.

Getting Started

It all starts with a very simple conversation. For each

client, determine the following four numbers with regard

to life insurance:

•

How much do they have? (Shockingly, many don’t know.)

•

How much do they need?

•

How much can they get?

•

How much do they want?

From there, you need to know about any health issues the

client has—simply asking what medications he or she takes

can be an easy way to find out. Then, the Insurance team

will work with you on a proposal. Note that several carriers

will write up to $250,000 without paramedical exams,

with that number expected to rise to $1 million in 2014.

“How much do you want?”

At our 2013 National

Conference, Penn Mutual’s Allan Sternberg talked about

the value of insuring clients for the most they can get.

Throughout his career, Allan has used the following chart

(Figure 2), showing the amount of coverage a client can

get as a multiple of income at each age. His message to

clients is straightforward: “Here’s how much you can get;

how much do you want?”

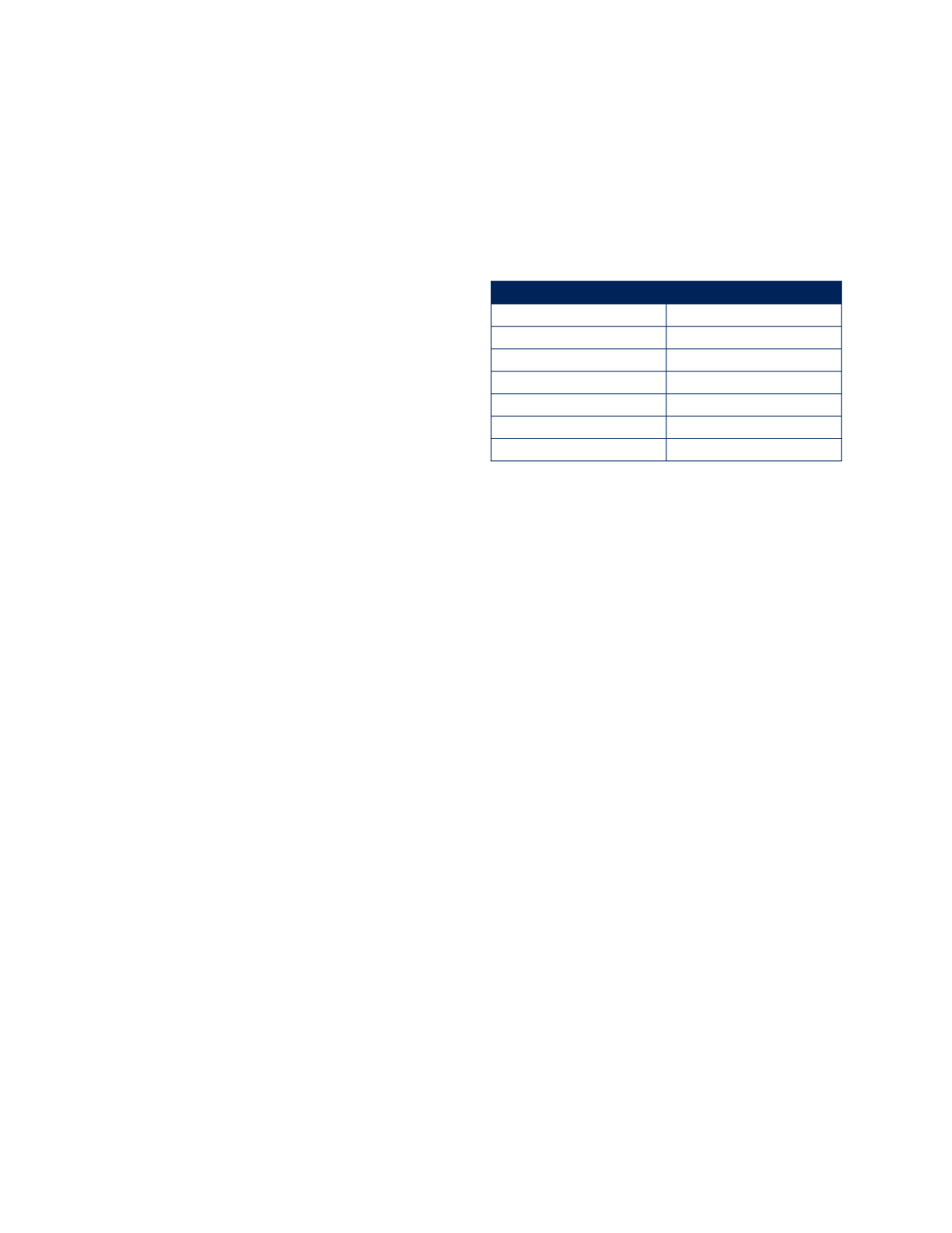

Figure 2. Insurance Coverage Available by Age

Age

Income Factor

18–30

30x

31–40

25x

41–50

20x

51–60

15x

61–70

10x

71+

Individual consideration

Allan also shared a personal story that brought the point

home. He was sitting on a flight when an alarm rang out,

the cabin filled with smoke, and the pilots began preparing

for an emergency landing. After making what could have

been his final phone call home, he felt at peace knowing

that, no matter what happened, his family would be taken

care of because he’d maxed out his life insurance coverage.

True Peace of Mind

“Peace of mind” is the ultimate goal of many financial

planning activities. But truthfully, with many aspects of

planning (particularly those with long time horizons), the

variability of results prevents a true feeling of security.

With the risk management aspect of a plan, however, you

can make a real promise to your clients and their families,

locking in security if the worst happens.

Remember, it’s at the top of the arc that your clients need

you most.

Brian Harrison is the director of insurance and

financial planning marketing. He is available at x9174 or

at