Wealth Management

/ Investments & Research

commonwealth.com

For Advisor Use Only

19

Decades of bad habits can wreak havoc on an individual’s

long-term plans, and decisions made in an investor’s 20s

and early 30s may have more of an impact on his or her

golden years than most people realize.

Unfortunately, young investors are often undereducated

about how to approach investing and accumulating sufficient

assets for retirement. And this problem is intensifying as

industries move from defined-benefit structures toward

defined-contribution frameworks. Now, more than ever,

young investors hold the keys to their own financial futures.

It’s our job as analysts and advisors to provide much-needed

tutelage to inexperienced clients. Here we address a few

of the major issues that disproportionately affect fledgling

investors and provide food for thought for advisors who

may be spending the majority of their time working with

the older demographics.

Compounding Is a Young Investor’s

Best Friend—and a Benefit to Advisors

Albert Einstein once quipped that “compound interest is

the most powerful force in the universe.” Most advisors and

clients would likely agree with his assertion that a longer

time horizon allows investments to grow due to the effect

of compounding. The sheer scale of this benefit is best

demonstrated by way of an illustration.

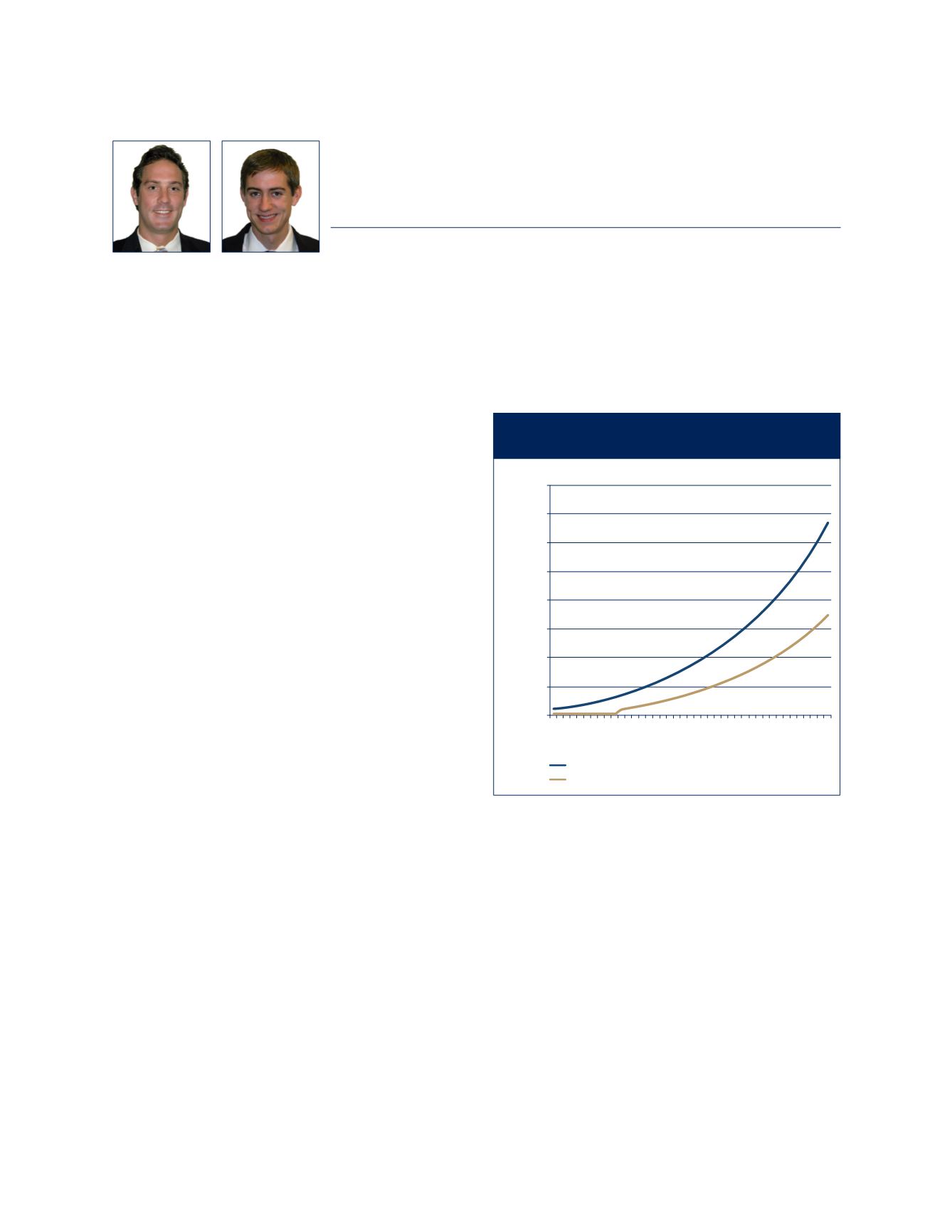

We compared the hypothetical portfolio growth of two

young clients. Both investors begin with $20,000 up front,

and both contribute $3,000 per year to their portfolios

until retirement; Client A, however, starts investing this

year, while Client B waits 10 years before starting to invest.

Using simple arithmetic, we would expect Client A to end

up with $30,000 (i.e., $3,000 x 10 years) more in the

bank at retirement than Client B. But that doesn’t take

compounding into account.

Let’s assume that both clients’ investments grow at a

6-percent rate. Because of compounding, after 40 years

have elapsed, Client A will actually end up with nearly

double the assets of Client B, simply because she took the

initiative to start saving and investing earlier (see Figure 1).

This exponential growth of investable assets not only

benefits clients, but also helps advisors, who will likely garner

higher fee-based revenues. For example, after 13 years, Client

A’s $20,000 portfolio would grow to nearly $100,000, and,

after 22 years, it could reach $200,000.

Because younger investors on average have a higher ability

to take risk, advisors can expect the value of their portfolios

to potentially grow at a faster rate. This could be helpful

Longevity and the Power of Compounding

Make Younger Investors a Unique Opportunity

PETER ESSELE, CFA®, AND SEAN FULLERTON, CFA®

Many investors believe that the most important period for wealth accumulation is

the one leading up to retirement, when they are at the peak of their earnings cycles.

But we would argue that the period when one enters the labor force is equally

important, if not more so.

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$670,000

Growth of Investments

$352,044

2014

2017

2020

2023

2026

2029

2032

2035

2038

2041

2044

2047

2050

2053

Start This Year

Start 10 Years from Now

Source: Commonwealth

Figure 1. Performance Comparison of Two

Hypothetical Investors Over 40 Years